My son went on his first date this weekend. He and this girl have been going to school with each other for years. In fact, they were the lead roles in a school play back in grade school. Anyway, they’ve been flirting for a while and he mustered up the courage to ask her to be his girlfriend…I guess he just walked up to her in school and asked. She initially rejected the idea saying she just wanted to be friends, but the next day she reconsidered and asked him if the offer was still on the table. The next thing ya know they’re going to a movie and getting Cane’s together. I gotta say, it’s pretty cool…he’s way ahead of me when I was that age…I didn’t get up the courage to ask a girl out until my freshman year in college. My wife and I did a good job…he’s got that right balance of humility, respect, and confidence. In fact, he’s beaming with confidence but why shouldn’t he be? He’s bigger, stronger, faster, and smarter than I ever was.

Survey Results – Reasons An MCA Lender Declines A Merchant & WBL’s Ability To Overcome

I sent this survey only to my approved ISOs/Brokers. There were 43 responses to the question within a week or so. FYI, a few of the responses included reasons the MCA loan failed to fund, like the Merchant didn’t provide the requested documentation, but this implies the MCA was initially approved so it doesn’t really answer the question I was asking.

Thanks to all who responded…here are the results in order of the most common responses:

1 Poor Cash Flow – not enough deposits/revenues in general or for a specific industry.

- WBL has a subsidy program to lower payments and an Interest Reserve program to use loan proceeds to cover the payments if necessary. Put another way, lack of cash flow DOES NOT RESTRICT WBL FROM LENDING.

2 Declining Deposits/Revenues. – three or more consecutive months of notable decline

- Although WBL would like an explanation why deposits/revenues are declining, as long as they are sufficient to support the debt, we’re still lending. That is, a Merchant with declining deposits/revenues is PERFECT FOR WBL.

3 Defaults – too many on past loans.

- If there is equity in real estate and the Merchant can illustrate they can afford the payments, then defaults on other loans IS A CHALLENGE WBL CAN OVERCOME.

4 Stacked MCAs. – too many open MCAs; overleveraged

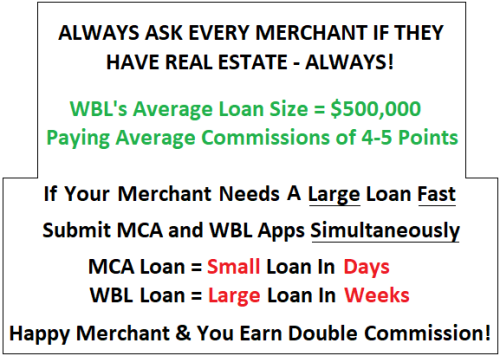

- WBL is not an MCA lender. Rather, we make loans to businesses securing real estate as collateral. That means we do not count in the stack of MCA loans. Moreover, having multiple MCA loans is a good thing for us because our ISO’s come to us to take out the MCA loans to lower the Merchant’s daily or weekly payments. Not only do we make a large loan to these Merchants, by paying off existing MCA debt we put the Merchant in a much stronger financial position, and, if needed, it makes more room for the ISO to make more loans. So, STACKED MCA DEBT IS IDEAL FOR A WBL TAKEOUT!

5 Borrowers’ Picture On DL Too Ugly – no, this one isn’t real…it’s my way of sneaking in a little humor.

6 Low Credit Score, BKs, Foreclosures, & Judgements

- We’ve been known to lend on a Fico score as low as 470 and we’re more interested in the equity of the real estate collateral and the Merchant’s ability to afford the loan payments, so most of the time, this is NOT AN ISSUE FOR WBL.

7 Time In Business Too Short – for a new business or they haven’t been doing it long enough.

- As long as the Merchant has sufficient revenues to support the debt, the length of time in the business bears little weight. For a start-up company, signed contracts for future revenue can be adequate to qualify and until the revenue is realized, we can put in place an Interest Reserve to cover payments. So, time in business DOES NOT RESTRICT WBL FROM LENDING.

8 High Risk Industry – I don’t know what this means but there were a few responses.

- Simply put, WBL DOES NOT DISCRIMINATE BASED ON THE INDUSTRY. There are some exceptions to this rule, for example, WBL does not lend to the cannabis industry or religious institutions.

Resource Links, Process & Loan Intake Instructions

Appointment Link – Get On Phil’s Calendar.

White Label Marketing Flyers Using Your Logo & Contact Information.

Flyer For Independent Sales Organization – ISO — Phil Grossfield

Email the Loan Opportunity To Me. Send me (1) an Application with all the Merchant/Borrower’s information including their mobile number and email address, (2) a full description of the real estate (download this Excel REO Schedule), and (3) a minimum 3-months business bank statements (6 months is better if you have it).

To Qualify For A Business Loan. (1) Equity in Real Estate – we’ll utilize virtually any type and combination of real estate in any condition, and (2) Revenues – sufficient to support/afford the loan payments. If we have these two, we can overcome just about any hurdle…

Process. After I send the loan opportunity to our Intake Department, they’ll send me feedback on the real estate collateral, affordability, and any other considerations. On the same day or next, I’ll present potential loan structures to our Market Clearance team for guidance. Then you and I will discuss and decide what to Offer your Merchant Borrower. If accepted, then we’ll send the an authorization form and formally submit the loan.

Always Ask Merchant/Borrower If They Have Real Estate – What Real Estate Will Be Acceptable As Collateral?