I Miss Coaching Baseball. Prior to Covid I coached 7 years in Little League for my son. My father-in-law (shown with me and my son to the right) was my assistant coach. We taught and motivated the kids to play at a high level, but more importantly to have fun doing it. Sounds easy enough but there were a lot of Dad’s who were coaching for themselves rather than for the kids…too much yelling and seriousness reminiscent of Coach Turner in The Bad News Bears. Our philosophy was to ensure the kids had a good time so they wanted to keep playing baseball rather than sit in front of a computer. When Covid hit they shut the league down and my son lost interest. And just like that my career as a coach was over. I miss the fields.

Double Commissions

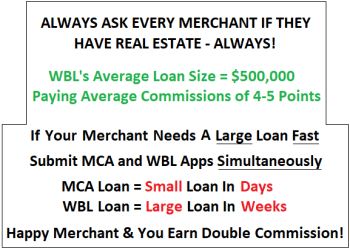

First, we are not an MCA lender…we’re a commercial business lender securing loans with real estate which means our loans don’t count in the stack of MCA loans. But ISOs send us a lot of business…here’s just one of many reasons why. Let’s assume your Merchant needs a large loan fast.

With an MCA loan, you get the money fast but you’re limited in loan size based on revenues. But WBL loans are based on the equity in real estate so our loan amounts average $500,000 and go up to $2m. The rub is that our loans take longer to close because we have to get a title and valuation report on the real estate.

SO THIS IS WHAT YOU DO…get the Merchant an MCA loan now for whatever loan amount you can get approved, AND SIMULTANEOUSLY, submit to WBL for a much larger loan amount. Your Merchant will be happy because they’ll get some funds quickly and in just a few weeks they’ll get a whole lot more…WIN-WIN! In the meantime, you’ll earn a commission on the MCA loan quickly and another commission from WBL when our loan closes. HERE’S WHAT I NEED YOU TO DO:

(1) Look through your recently funded MCAs to see if your Merchants have real estate because if they do, there’s another potential commission just waiting for you! (2) Look for MCAs you lost because the loan was not enough for the Merchant…if they have real estate there’s a potential commission just waiting for you! (3) Look for MCA loans you lost because the Merchant was already stacked…if they have real estate there’s a potential commission just waiting for you! (4) Look for MCA loans you lost for some other reason…if they have real estate we can overcome almost any challenge, and guess what…yep, there’s a potential commission just waiting for you! One last thing…WHEN SPEAKING TO A MERCHANT FOR THE FIRST TIME, ALWAYS ASK IF THEY HAVE REAL ESTATE…ALWAYS! If they do, I’m your first call…

Previously: NO PAYMENT & SUBSIDIZED PAYMENT BUSINESS LOANS

The Market…My Take

Will The Fed Hike Rates Again? Maybe…probably. The Fed raised their Fed Funds Rate several times in 2022 to battle inflation (to learn more about that, read this). But whether the recent rate hikes are working to lower the prices of consumer goods is yet to be seen. In virtually every category prices have gone up and I don’t know about you, but I haven’t seen any relief. Until stores start lowering prices, you can count on the Fed to continue to raise the Fed Funds rate. My friends in the residential mortgage business have gotten excited to see mortgage rates stabilize and even reduce a little in the last couple of weeks. But I think this is simply a reaction to some of the big players lowering their rates to buy the market and the smaller guys lowering their rates to try and compete. So from my perspective I don’t think that’s any indication of the current war on inflation. How does this affect the business loan market? Just like everyone else. You can expect business loan rate to follow suit and increase. Let me know your thoughts on this subject…I love hearing your opinions on the markets…

Previously: How Does Raising Fed Interest Rates Battle Inflation? | Good Time To Hire Salespersons

Resource Links, Process & Loan Intake Instructions

Appointment Link – Get On Phil’s Calendar.

White Label Marketing Flyers Using Your Logo & Contact Information.

Flyer For Independent Sales Organization – ISO — Phil Grossfield

Email the Loan Opportunity To Me. Send me (1) an Application with all the Merchant/Borrower’s information including their mobile number and email address, (2) a full description of the real estate (download this Excel REO Schedule), and (3) a minimum 3-months business bank statements (6 months is better if you have it).

To Qualify For A Business Loan. (1) Equity in Real Estate – we’ll utilize virtually any type and combination of real estate in any condition, and (2) Revenues – sufficient to support/afford the loan payments. If we have these two, we can overcome just about any hurdle…

Process. After I send the loan opportunity to our Intake Department, they’ll send me feedback on the real estate collateral, affordability, and any other considerations. On the same day or next, I’ll present potential loan structures to our Market Clearance team for guidance. Then you and I will discuss and decide what to Offer your Merchant Borrower. If accepted, then we’ll send the an authorization form and formally submit the loan.

Always Ask Merchant/Borrower If They Have Real Estate – What Real Estate Will Be Acceptable As Collateral?