NO LABOR FOR LABOR DAY

NO LABOR FOR LABOR DAY

The concept of Labor Day was to honor and recognize the contributions of laborers to the achievements of the United states…at least that’s what is was in 1894. I find it ironic that we celebrate Labor Day this year and have such a shortage of labor because apparently people don’t want to go back to work. Isn’t that counter-intuitive since the cost of living has risen so steeply with inflation? What exactly is going on? Why do I see restaurants with closed off sections because they don’t have enough workers? Why do I see businesses with restricted hours or that shut down periodically for the same reason? Why is it that every support department excuse for bad service is that there aren’t enough employees?  Is it because people are afraid of COVID and don’t want to go to the store, or restaurant, or office? Or is Covid making it harder for people to return to work, like for parents whose kids are kept out of school frequently and the cost of childcare has skyrocketed? Is it because people have extra savings and/or are retiring earlier and don’t need to work? Is it because people just don’t see the value in working anymore…that the money is outweighed by their freedom particularly since wages aren’t enough to pay for everything anyway? I mean, are the benefits of not working outweighing working? But how do people afford to live…to eat? Really, I want to know…what is going on out there…why doesn’t anyone want to work and how are they surviving?

Is it because people are afraid of COVID and don’t want to go to the store, or restaurant, or office? Or is Covid making it harder for people to return to work, like for parents whose kids are kept out of school frequently and the cost of childcare has skyrocketed? Is it because people have extra savings and/or are retiring earlier and don’t need to work? Is it because people just don’t see the value in working anymore…that the money is outweighed by their freedom particularly since wages aren’t enough to pay for everything anyway? I mean, are the benefits of not working outweighing working? But how do people afford to live…to eat? Really, I want to know…what is going on out there…why doesn’t anyone want to work and how are they surviving?

No Payments & Reduced Payments – Subsidies & Interest Reserves

Let’s say your Merchant has limited revenues and it’s preventing you from getting them an MCA loan amount they need. But you were smart! You discovered they own real estate and called me! I offer your Merchant a MUCH LARGER LOAN AMOUNT and apply a subsidy or an interest reserve to overcome the limited deposits/revenues. So, what exactly is a subsidy and interest reserve and how does it work?

SUBSIDY: a subsidy reduces the monthly payment by splitting the subsidy amount over a period of time.  For example, if we build in a subsidy amount of $24,000 for 12 months, then we can reduce the regular monthly payment by $2,000/month for 12 months. Obviously this makes the loan payments more affordable for the Merchant.

For example, if we build in a subsidy amount of $24,000 for 12 months, then we can reduce the regular monthly payment by $2,000/month for 12 months. Obviously this makes the loan payments more affordable for the Merchant.

INTEREST RESERVE: an interest reserve covers the entire monthly pavement for a period of time. For example, if we build in an interest reserve amount of $24,000, and the regular payments are $4,000 per month, then for the first 6 months of the loan the Merchant’s payments are covered entirely and they don’t have to make a payment until month 7. This gives them time to build up their revenues.

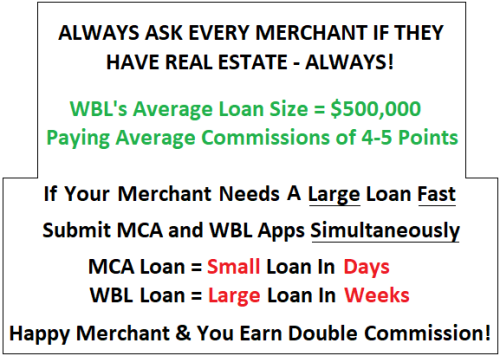

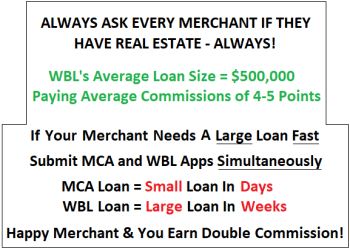

That’s why it’s so important you ask every merchant whether they have real estate. ALWAYS ASK EVERY MERCHANT WHETHER THEY HAVE REAL ESTATE! In fact, you should investigate whether merchants whom you’ve turned down or need more money have real estate.

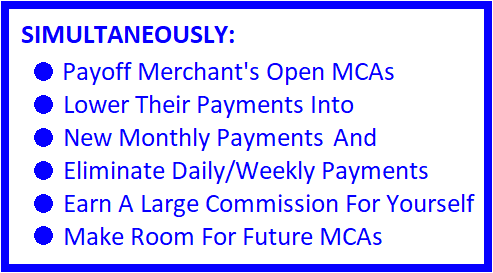

Consolidate MCA Loans Using Property & Earn Large Commissions

Payoff the Merchant’s open MCAs, lower their payments, make the new payments monthly instead of daily/weekly, earn a large commission for yourself, and make room for more MCA loans in the future…and do it all simultaneously.

How’s that sound? WBL loans are not considered MCA loans, rather, we make loans to businesses using real estate as collateral. That’s why it’s so important you ask every merchant whether they have real estate. In fact, you should investigate whether merchants whom you’ve already funded have real estate ,,, I guaranty there are loans right in front of you that you didn’t even realize were there. Moreover, with real estate, we can overcome most issues that resulted in a declined MCA loan. And if your Merchant was looking for more cash but you were limited by an MCA loan, there’s likely a much larger loan amount available if they have real estate. ALWAYS ASK EVERY MERCHANT WHETHER THEY HAVE REAL ESTATE!

How’s that sound? WBL loans are not considered MCA loans, rather, we make loans to businesses using real estate as collateral. That’s why it’s so important you ask every merchant whether they have real estate. In fact, you should investigate whether merchants whom you’ve already funded have real estate ,,, I guaranty there are loans right in front of you that you didn’t even realize were there. Moreover, with real estate, we can overcome most issues that resulted in a declined MCA loan. And if your Merchant was looking for more cash but you were limited by an MCA loan, there’s likely a much larger loan amount available if they have real estate. ALWAYS ASK EVERY MERCHANT WHETHER THEY HAVE REAL ESTATE!

Resource Links, Process & Loan Intake Instructions

Appointment Link – Get On Phil’s Calendar.

White Label Marketing Flyers Using Your Logo & Contact Information.

Flyer For Independent Sales Organization – ISO — Phil Grossfield

To Qualify For A Business Loan. (1) Equity in Real Estate – we’ll utilize virtually any type and combination of real estate in any condition, and (2) Revenues – sufficient to support/afford the loan payments. If we have these two, we can overcome just about any hurdle…

Email the Loan Opportunity To Me. Send me (1) an Application with all the Merchant/Borrower’s information including their mobile number and email address, (2) a full description of the real estate (download this Excel REO Schedule), and (3) a minimum 3-months business bank statements (6 months is better if you have it).

Process To Get Started. After I send the loan opportunity to our Intake Department, they’ll send me feedback on the real estate collateral, affordability, and any other considerations. On the same day or next, I’ll present potential loan structures to our Market Clearance team for guidance. Then you and I will discuss and decide what to Offer your Merchant Borrower. If accepted, then we’ll send the an authorization form and formally submit the loan.

Always Ask Merchant/Borrower If They Have Real Estate – What Real Estate Will Be Acceptable As Collateral?

First, this might be a spoiler so if you haven’t watched it yet on HBO I encourage you to do so, but don’t read any further here. In my opinion, Game of Thrones may be the best series ever, maybe with the exception of Breaking Bad. I just finished watching the entire GOT series for the second time in anticipation of the new series entitled House Of The Dragon which just started. That said, MANY people were upset with GOT’s ending after 8 seasons, including me. The main consensus was that the writers rushed the last season and failed to properly develop Daenerys Targaryen’s character before she went completely dark and torched King’s Landing.

First, this might be a spoiler so if you haven’t watched it yet on HBO I encourage you to do so, but don’t read any further here. In my opinion, Game of Thrones may be the best series ever, maybe with the exception of Breaking Bad. I just finished watching the entire GOT series for the second time in anticipation of the new series entitled House Of The Dragon which just started. That said, MANY people were upset with GOT’s ending after 8 seasons, including me. The main consensus was that the writers rushed the last season and failed to properly develop Daenerys Targaryen’s character before she went completely dark and torched King’s Landing.  HOWEVER, after watching the series again, I now feel better about it having realized they did provide several hints to her destructive nature leading into the final season. Just before she goes bonkers her first dragon was murdered and she lost half her army fighting the Night King. Then, shortly thereafter her second dragon was murdered and her best friend was beheaded right in front of her by Cersei Lannister. At this point she understandably lost her blank. So, although I wish they had revealed her monstrous character more profoundly and earlier, you can rest easy knowing I’ve forgiven the writers. Now, on to House Of The Dragon!.

HOWEVER, after watching the series again, I now feel better about it having realized they did provide several hints to her destructive nature leading into the final season. Just before she goes bonkers her first dragon was murdered and she lost half her army fighting the Night King. Then, shortly thereafter her second dragon was murdered and her best friend was beheaded right in front of her by Cersei Lannister. At this point she understandably lost her blank. So, although I wish they had revealed her monstrous character more profoundly and earlier, you can rest easy knowing I’ve forgiven the writers. Now, on to House Of The Dragon!.

My Dad was a couple weeks shy of 80 years before he passed last week. He battled Alzheimer’s for the better of 20 years…the last 5 years were extremely challenging. His unyielding positive attitude was Dad’s best characteristic and he never lost it despite the efforts of the viscous disease. He was (and remains) my moral compass and set an example of the highest work ethic which is what made him the #1 salesperson for 40 years with Champion Products sportswear. With his guidance I became a record-setting salesperson myself and came to appreciate the dedication required to achieve that level of success.

My Dad was a couple weeks shy of 80 years before he passed last week. He battled Alzheimer’s for the better of 20 years…the last 5 years were extremely challenging. His unyielding positive attitude was Dad’s best characteristic and he never lost it despite the efforts of the viscous disease. He was (and remains) my moral compass and set an example of the highest work ethic which is what made him the #1 salesperson for 40 years with Champion Products sportswear. With his guidance I became a record-setting salesperson myself and came to appreciate the dedication required to achieve that level of success.

Popular Vote versus Electoral Vote – Explained. The popular vote is simply the number of Americans voting for a particular candidate. But the electoral vote is much more complicated. It’s actually the House members of each state that cast the actual votes based on how the citizens of that state vote. Each state has 2 U.S. Senators and a number of House of Representatives based on the state’s population. For example, California has 2 Senators and 53 House members for a total of 55 votes because its population is huge compared to Arizona who has 2 senators and 7 House members for a total of 9. The idea was to balance the voting power to the smaller states.California has about 40 million people and Arizona has about 7 million. Each member of the House represents about 725,000 people in California (40m/55) whereas each member of the House in Arizona represents about 775,000 (7m/9). Many think this it’s unfair that the candidate that won the popular vote should get trumped by the winner of the electoral vote (pun intended).

Popular Vote versus Electoral Vote – Explained. The popular vote is simply the number of Americans voting for a particular candidate. But the electoral vote is much more complicated. It’s actually the House members of each state that cast the actual votes based on how the citizens of that state vote. Each state has 2 U.S. Senators and a number of House of Representatives based on the state’s population. For example, California has 2 Senators and 53 House members for a total of 55 votes because its population is huge compared to Arizona who has 2 senators and 7 House members for a total of 9. The idea was to balance the voting power to the smaller states.California has about 40 million people and Arizona has about 7 million. Each member of the House represents about 725,000 people in California (40m/55) whereas each member of the House in Arizona represents about 775,000 (7m/9). Many think this it’s unfair that the candidate that won the popular vote should get trumped by the winner of the electoral vote (pun intended). Many argue that a much higher percentage of people in the country would vote if we moved away from the electoral process.

Many argue that a much higher percentage of people in the country would vote if we moved away from the electoral process. The point is, if we used the popular vote, the overall strategies of the campaigns, where they visited, the speeches, the advertisements, everything would be different. Clinton may have lost by 20 million or won by 50 million…there’s no way to know. So when anyone makes an argument that Trump would have lost or Clinton should have won, it’s nonsense. Unless we actually change the system, we’ll never know the true impact to the election results.

The point is, if we used the popular vote, the overall strategies of the campaigns, where they visited, the speeches, the advertisements, everything would be different. Clinton may have lost by 20 million or won by 50 million…there’s no way to know. So when anyone makes an argument that Trump would have lost or Clinton should have won, it’s nonsense. Unless we actually change the system, we’ll never know the true impact to the election results.